Bookkeeping

Direct Labor Variances Formula, Types, Calculation, Examples

If materials and tools are readily available and in good condition, workers can perform tasks more efficiently, resulting in favorable variances. Shortages or poor-quality tools can hinder productivity, causing unfavorable variances. By analyzing labor rate variance, companies can determine if they are paying more or less for labor than expected and identify areas where wage cost control measures may be needed. Actual labor costs may differ from budgeted costs due to differences in rate and efficiency. One of the best ways to monitor labor efficiency is, for sure, using time-tracking software. For example, advanced tools like SmartBarrel’s workforce management solutions provide real-time insights into labor usage on the construction site.

- Hitech manufacturing company is highly labor intensive and uses standard costing system.

- To calculate Direct Labor Mix Variance you must first identify the exact amount of labor it requires to produce a product.

- According to the total direct labor variance, direct labor costs were $1,200 lower than expected, a favorable variance.

- Understanding labor efficiency variance helps companies identify inefficiencies in their production processes and take corrective actions to improve labor productivity.

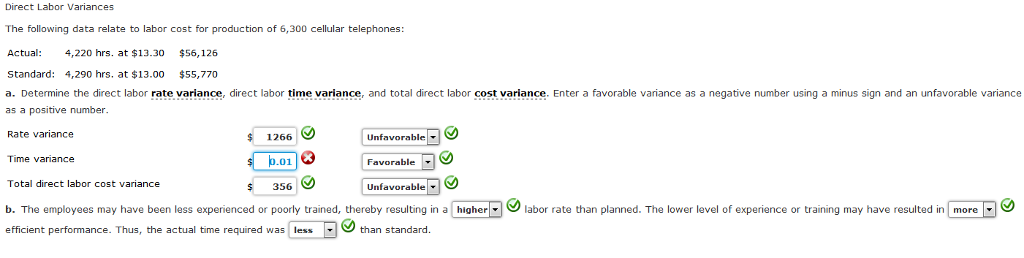

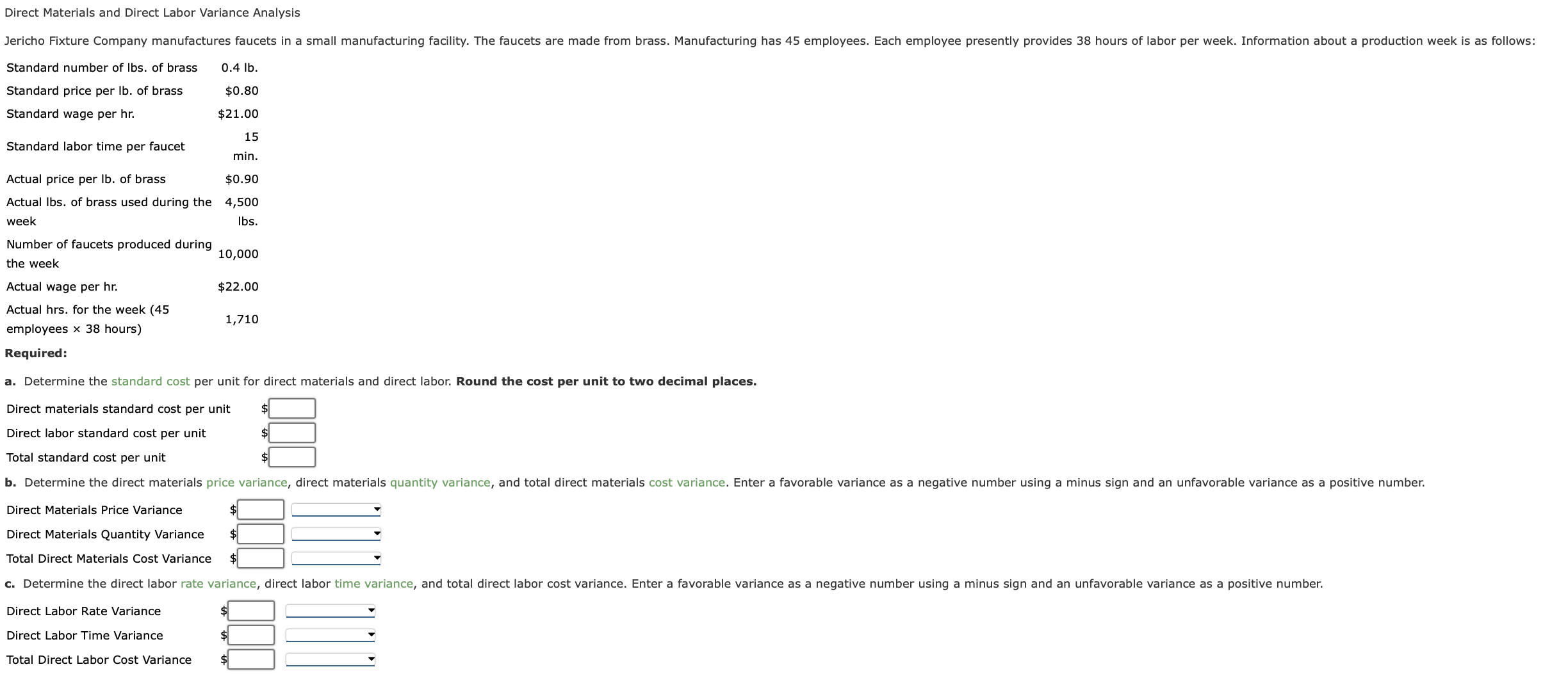

Direct Labor Variances

Labor rate variance arises when labor is paid at a rate that differs from the standard wage rate. Labor efficiency variance arises when the actual hours worked vary from standard, resulting in a higher or lower standard time recorded for a given output. An adverse labor rate variance indicates higher labor costs incurred during a period compared with the standard.

How do you calculate labor yield variances?

The difference column shows that 100 extra hours were used vs. what was expected (unfavorable). It also shows that the actual rate per hour was $0.50 lower than standard cost (favorable). The total actual cost direct labor cost was $1,550 lower than the standard cost, which is a favorable outcome. The difference in hours is multiplied by the standard price per hour, showing a $1,000 unfavorable direct labor time variance.

Direct Labor: Standard Cost, Rate Variance, Efficiency Variance

In order to keep the overall direct labor cost inline with standards while maintaining the output quality, it is much important to assign right tasks to right workers. In other words, when actual number of hours worked differ from the standard number of hours allowed to manufacture your property taxes a certain number of units, labor efficiency variance occurs. With either of these formulas, the actual hours worked refers to the actual number of hours used at the actual production output. The standard hours are the expected number of hours used at the actual production output.

Case Study 1: Company A’s Experience with Labor Rate Variance

If the direct labor cost is $6.00 per hour, the variance in dollars would be $0.90 (0.15 hours × $6.00). For proper financial measurement, the variance is normally expressed in dollars rather than hours. Direct labor rate variance determines the performance of human resource department in negotiating lower wage rates with employees and labor unions. A positive value of direct labor rate variance is achieved when standard direct labor rate exceeds actual direct labor rate. Thus positive values of direct labor rate variance as calculated above, are favorable and negative values are unfavorable.

To compute the direct labor price variance, subtract the actual hours of direct labor at standard rate ($43,200) from the actual cost of direct labor ($46,800) to get a $3,600 unfavorable variance. This result means the company incurs an additional $3,600 in expense by paying its employees an average of $13 per hour rather than $12. To compute the direct labor quantity variance, subtract the standard cost of direct labor ($48,000) from the actual hours of direct labor at standard rate ($43,200). This math results in a favorable variance of $4,800, indicating that the company saves $4,800 in expenses because its employees work 400 fewer hours than expected.

By regularly analyzing labor variances, businesses can identify opportunities for improvement and ensure that they are making the most efficient use of their labor resources. Doctors, for example, have a time allotment for a physical exam and base their fee on the expected time. Insurance companies pay doctors according to a set schedule, so they set the labor standard. In this question, the Bright Company has experienced a favorable labor rate variance of $45 because it has paid a lower hourly rate ($5.40) than the standard hourly rate ($5.50). Monitoring labor hours is as important as comparing them to the standard hours allowed. Thanks to this, your projects will stay on time and, probably more important than that, they’ll be within budget.

DLYV can be affected by several factors, such as labor rate or wage changes, variations in employee skill levels, differences in the number of hours worked, and changes in working conditions. Labor hours used directly upon raw materials to transform them into finished products is known as direct labor. This includes work performed by factory workers and machine operators that are directly related to the conversion of raw materials into finished products. This formula gives you a clear picture of how much the actual labor usage deviated from the budgeted amount. A positive result indicates greater efficiency (i.e., less time was needed), while a negative result highlights inefficiencies (more time was used than planned).

Direct labor rate variance is equal to the difference between actual hourly rate and standard hourly rate multiplied by the actual hours worked during the period. The variance would be favorable if the actual direct labor cost is less than the standard direct labor cost allowed for actual hours worked by direct labor workers during the period concerned. Conversely, it would be unfavorable if the actual direct labor cost is more than the standard direct labor cost allowed for actual hours worked. In this case, the actual rate per hour is $9.50, the standard rate per hour is $8.00, and the actual hours worked per box are 0.10 hours.